I Bought a Vest

I bought a vest a few weeks ago. Like all boring men in finance, I love a good vest in the winter. This year I decided to expand my vest collection, so I went to the website of America’s most reliable retailer, LL Bean, and found one that matched with navy slacks (I told you I’m boring). Then, about a week later, I got snagged in a social media ad and bought another vest! It was officially a spree.

I got it in the mail, tried it on, then hung it up in my closet. But as I slipped that coat hanger onto the rail, it triggered a strong memory. Next to my new vest was an older vest I had bought eight years ago at the Cool Springs Mall. I remember paying about $80 at a time when that was a somewhat significant amount of money for me to spend on something superfluous. Seeing it in my closet reminded me of how good that purchase felt at the time. It fit well, it looked good, and I was proud to own something from a nice brand name.

As I looked at those two vests, I compared how I felt when I purchased each of those items. It was night and day. My new vest didn’t give me nearly the same kind of pride and enjoyment that I felt 8 years ago. Honestly, it felt no different than getting a pair of socks in the mail.

Why is that? Both pieces of clothing cost about the same. They were of the same quality. And they would be used the same way. Why did one of those purchases make me feel so much better? I’ll steal a quote from author Morgan Housel to help explain, since he spurred so much of my thinking on this topic.

“There is no such thing as an objectively good experience. Every amount of good is just the gap between expectations and reality. It’s the distance between what you have now and what you had before. The contrast, not the amount, is what makes you happy “

So why did the two purchases feel so different to me? It was all about contrast. First, buying something for the first time feels a lot more powerful than buying it for the third, fourth, or fifth time. After all, who do you think gets more pleasure at a football game? The man in the box seats attending his 300th game? Or the little boy in the nosebleeds seeing his first game?

Secondly, it felt better because of how different the contrast in sacrifice was. That first vest was a real sacrifice in my budget. I remember standing in the store with Toria, haggling with myself over the decision. My most recent purchase? I didn’t think twice, and I’m still not sure my wife even knows I bought it.

So what does this mean for us (I say us because I need this lesson just as much as any of you)? The lesson here is that maybe it’s time we reevaluated the value of saying “I’ll pass” on a purchase. Obviously, there is a financial benefit to reducing your spending, and no one is saying you should hold off on paying for necessities. But there is an incredible amount of value in stopping to ask,

“What purchases are actually important to me?”

“What purchases actually make me happy?”

Holding off on certain expenses fills up a container inside of us. The more we hold off, the more enjoyment fills the container. So, when we finally do make that purchase, the container is emptied, and our joy is multiplied.

You likely already knew this to be true. Your bed feels the best after a week of sleeping on a hotel mattress. You’ve never had a glass of wine that tastes as good as a glass of tap water after a long day in the sun. And you’ve never loved your spouse more than when you’ve reconciled after a fight.

The joy we get from spending money varies for each of us, and it’s up to us to take the time to get to know ourselves. What really makes you tick? What really makes those long hours at work worth it? You’ve sacrificed for years to build your nest egg, so what’s a truly worthwhile way to spend it?

My challenge this week is to go through your bank statement and look at anything you bought that wasn’t a necessity. Did it make your heart race a little bit in a good way? Did it bring you, or maybe someone else, some joy? Or did it just give you that “bought some socks” feeling?

I hope we can go into this new year with a little more intentionality. I hope we can stop and ask ourselves, “Will this actually make me happy?” before we swipe the card. I know I need this lesson. I’ll end my thoughts here; I need to go look up the LL Bean return policy.

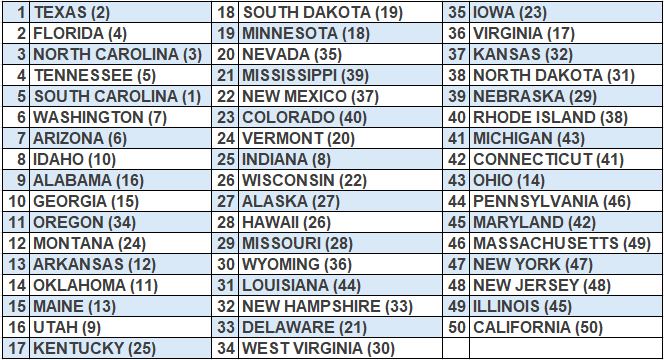

Chart of the Quarter

Each year, U-Haul releases a report detailing the flow of American's as they moved from one state to the other. The chart below ranks each state in terms of net growth. Texas lead the way with 50.7% of movers entering the state and 49.3% leaving the state. California came in last place as 49.4% moved in and 50.6% moved out.1

The 529 Account: More Than Just College Savings

While we mostly know 529 plans to be advantageous because of federal tax benefits, the first 529 plan was created in Michigan in 1986. Thank you to our Wolverine friends! While plans are still sponsored by each state, they were later added to IRS tax code as a federal item in 1996.

Many of the initial plans had a simple premise. You could get tax deferred growth and distributions as long as it was used for college tuition. The fear with these plans was always that the child might not use all or any of the funds set aside for their college education, and parents would be faced with taxes and penalties to make withdrawals.

However, since their inception, changes have been made to the rules that govern 529 plans and created opportunities to make withdrawals for more than just tuition. Encouragingly for savers, these opportunities have been spearheaded by both major political parties. These changes have mostly come as part of three large congressional bills in the past decade.

Note: While 529 plans might also carry state tax benefits in your state, we’ll be focusing on things from a federal tax perspective.

2017: Tax Cuts and Jobs Act

- K–12 Tuition: Up to $10,000 per year, per beneficiary, can be withdrawn from a 529 plan to pay for tuition at a public, private, or religious elementary or secondary school.

2023: Secure Act 2.0

- Roth Rollovers: The owner of a 529 (usually the parent) can roll over a sum equal to the Roth contribution maximum ($7,500 in 2026) into a Roth IRA for the beneficiary. This can be done for a maximum of 5 years for a total of $37,500. To do this, the 529 has been open for at least 15 years, and rollovers can’t exceed the amount of the contributions.

2025: OBBBA

- K-12 Education: The annual limit was increased to $20,000. Additionally, funds can be withdrawn for more than just tuition. Qualified expenses now include curriculum materials, fees for standardized tests, books, dual-enrollment course costs, online educational programs, and more.

- Credential Programs: Funds can now be used towards expenses that encourage lifelong learning. Qualified expenses now include Workforce Innovation and Opportunity- approved programs, credentials sanctioned by state or federal governments, military credentials, and certifications authorized by recognized professional providers.

This added flexibility means 529 Plans are now even more attractive to those looking to save for the next generation. While their education focus might not be a good fit for your family, we’d love a chance to discuss your options with you.

Team News

Our very own Kim Benefield recently completed her Retirement Income Certified Professional designation. The RICP® program required a large number of study hours and the passing of three difficult exams. With this designation, Kim is better equipped to help our clients plan to face the planning challenges that retirees face. Recently, Kim has also lent her knowledge to our firm as a member of the Registered Assistant Advisory Council. To put it simply, we don’t know what we’d do without her. Congratulations Kim!

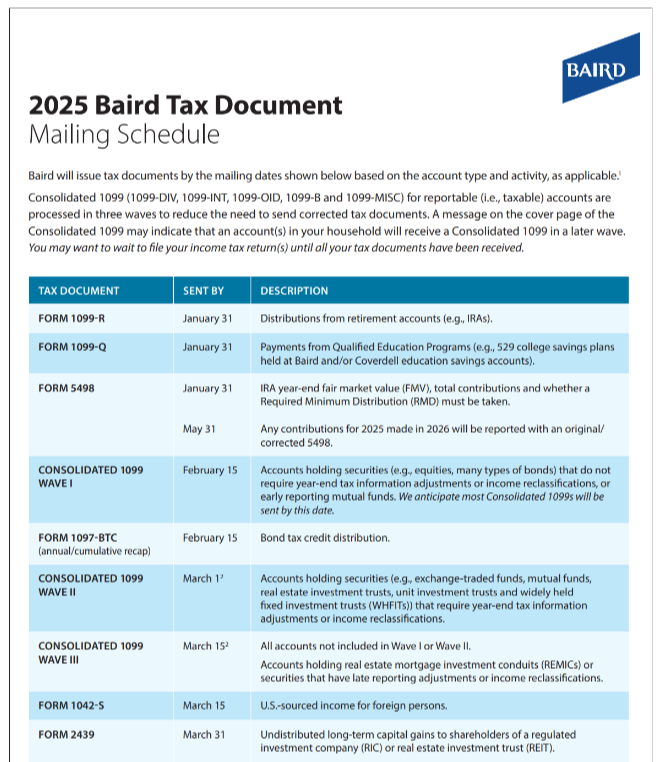

Baird Tax Doc Schedule

Market Wrap Up

Does this sound familiar? The stock market in 2025 ended strongly as global AI spending pushed everything from tech stocks to precious metals higher. It was truly the same song as 2024, but the second verse. Some estimate that $1.5 trillion dollars were spent on Artificial Intelligence infrastructure by corporations.

Behind the scenes, consumer spending continued to stay strong, though not strong enough to cause inflation to rebound. The Consumer Price Index (CPI) is expected to reflect that prices rose roughly 3% last year. While rising prices carry challenges, it’s a much more manageable rise than we’ve witnessed in recent years.

As previously discussed, much of the US stock market continues to be concentrated in a few names. While this concentration carries risk, many of those names also carry some of the strongest balance sheets, cash flow, and market share in the history of our economy. Alphabet (Google) and Nvidia led the way in 2025 with 65% and 40% returns, respectively.

The S&P 500 has now seen double-digit returns in 8 of the past 10 years. In 2026, we see reason for optimism that this trend can continue. Lower interest rates, low oil prices, and continued wage growth are all positive trends. However, unemployment is creeping up towards 5% and could be the cause for falling rents and somewhat weaker holiday spending numbers.

As a team, our goal is to bring you the best service and advice that we can in 2026. We’re thankful for your trust and business, and we hope this year is your best yet!

Sources and Disclosures

The information offered is provided to you for informational purposes only. Robert W. Baird & Co. Incorporated is not a legal or tax services provider and you are strongly encouraged to seek the advice of the appropriate professional advisors before taking any action. Investors should consider the investment objectives, risks, charges and expenses associated with a 529 Plan before investing. This and other information is available in a Plan’s official statement. The official statement should be read carefully before investing. Depending on your state of residence, there may be an in-state plan that provides tax and other benefits such as financial aid, scholarships and creditor protection that are not available through an out-of-state plan. Before investing in any state’s 529 plan, you should consult your tax advisor.

Fixed income is generally considered to be a more conservative investment than stocks, but bonds and other fixed income investments still carry a variety of risks such as interest rate risk, credit risk, inflation risk and liquidity risk. In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Municipal securities investments are not appropriate for all investors, especially those taxed at lower rates.

An investment in a money market mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency but is protected by SIPC coverage. Although money market mutual funds typically seek to preserve the value of an investment at $1.00 per share, there can be no assurance that will occur, and it is possible to lose money should the fund value per share fall. Most money market mutual funds are required to maintain a stable $1.00 net asset value per share, but some are not.

Investors should consider the investment objectives, risks, charges and expenses of each money market mutual fund carefully before investing. This and other information is found in the prospectus and summary prospectus. For a prospectus or summary prospectus, contact your financial advisor. Please read the prospectus or summary prospectus carefully before investing.

Rates are subject to change.

The calculation of the Standardized 30-Day Subsidized Yield is mandated by the SEC and is determined by dividing the net investment income per share earned during the period by the maximum public offering price of the Fund (“POP”) per share on the last day of the period. This number is then annualized.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index. Robert W. Baird & Co. Incorporated.

The information offered is provided to you for informational purposes only. Robert W. Baird & Co. Incorporated is not a legal or tax services provider and you are strongly encouraged to seek the advice of the appropriate professional advisors before taking any action. Investors should consider the investment objectives, risks, charges and expenses associated with a 529 Plan before investing. This and other information is available in a Plan’s official statement. The official statement should be read carefully before investing. Depending on your state of residence, there may be an in-state plan that provides tax and other benefits such as financial aid, scholarships and creditor protection that are not available through an out-of-state plan. Before investing in any state’s 529 plan, you should consult your tax advisor.